The market weakness we experienced this past week does not appear to be associated with any one event, but rather seems to be the result of a few factors.

- Uncertainty around the timing of Fed “lift-off” continues to give the markets concern; markets hate uncertainty, and this is a key area of confusion.

- The narrative around weaker growth in China, and emerging markets more broadly, has spilled over into commodity and currency markets, causing a new wave of risk-aversion.

- A general lack of economic data has created a bit of a news vacuum, causing increased focus on the aforementioned developments.

- Friday’s decline was 531 points in the DJIA, which was a loss of -3.1%. During this bull market there have been 11 similar daily declines of that size (or larger), and in every instance the market went on to new highs. So yesterday’s decline, by itself, does not mean we’re in a bear market.

- This week’s loss in the S&P 500 Index was -5.7%. Since 1940, there have been 38 weekly declines of this size (or larger). Surprisingly, there were 3 times as many double-digit gains three months later, than there were double-digit losses. So this week’s decline doesn’t necessarily indicate more big losses ahead.

- The market is now the most oversold since the 2011 correction lows. Historically, readings such as this indicate a high probability of a rally or bounce in the week ahead.

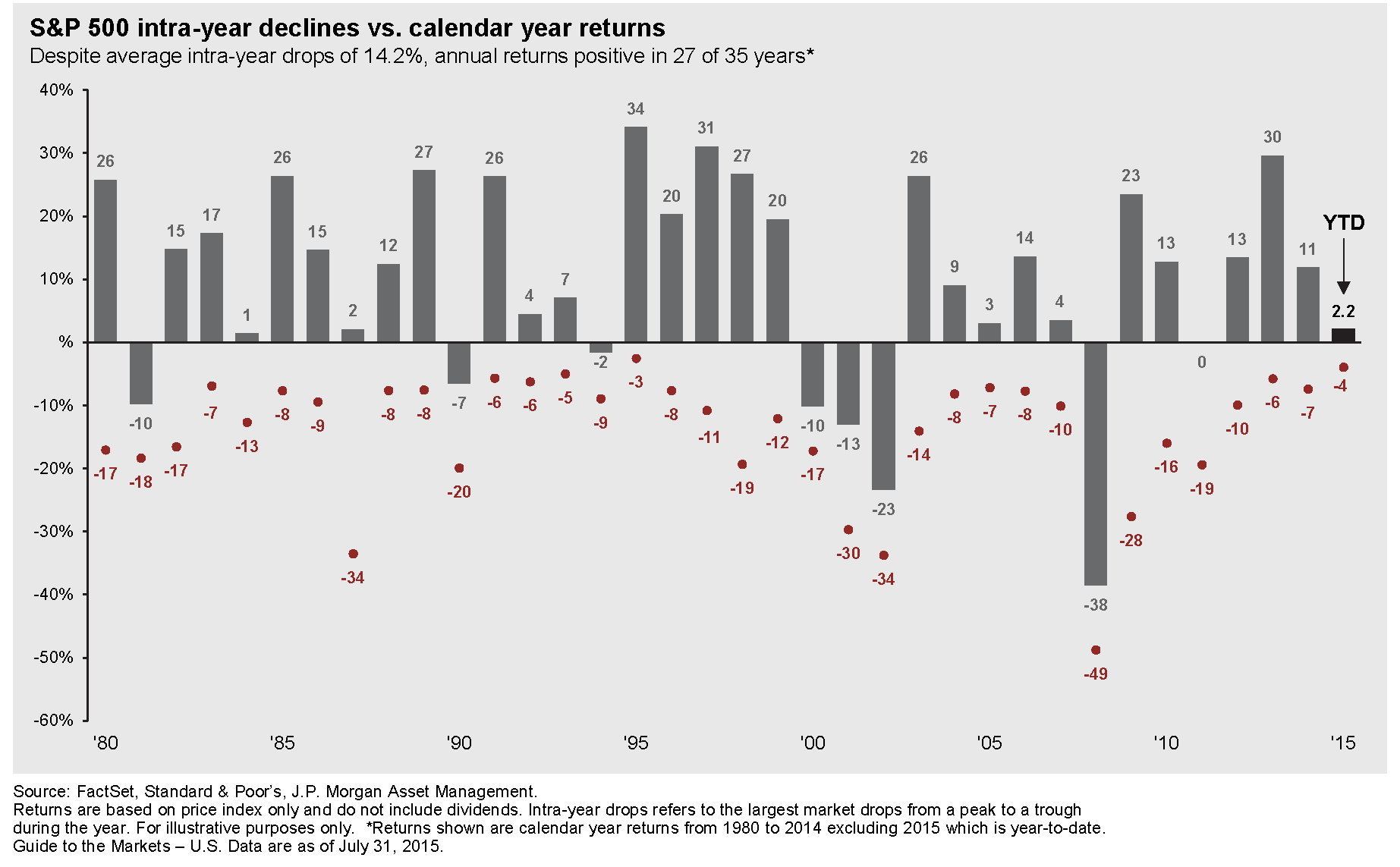

The last several years have been relatively calm for the U.S. stock market. For perspective, this 6+ year bull market has gone 1,418 calendar days without a 10% correction, which is the third longest such streak in the last half-century. After this week, the market (S&P 500) has now experienced an intra-year decline of -7.5% from its recent high. In reality, intra-year declines of 5% or worse are not unusual at all. In fact, it’s been 20 years since we experienced a year without at least a 5% decline.

The chart below illustrates a key point when it comes to market corrections. It shows intra-year stock market declines for the S&P 500 (red dot and number), as well as the market’s return for the full year (gray bar) since 1980. Note: the 2015 YTD return is through 7/31/15. The dots show the biggest peak-to-trough decline that occurred within each year. The dots are, in a sense, inevitable as the market doesn’t move in a straight line. Notice that the average annual peak-to-trough decline has been 14.2%. As these corrections occur each year, it’s normal for investors to get worried and wonder whether they should abandon the stock market all together. However, the reality is that in 27 of the last 35 years (77% of the time), the market has actually ended up for the year. What is clear is that the market is capable of recovering from intra-year drops and finishing the year in positive territory, which should encourage investors to stay the course when markets get choppy. In summary, history is heavily on the side of investors who don’t overreact to market corrections.

We’re not relaying these facts to downplay the market’s weakness (which technical indicators are confirming), but to convey that this correction may not be a full scale bear market. While there are some deep and growing concerns, we cannot say with certainty that we are in a bear market… at least not yet.

Because Friday closed on the low, we could very well see selling pressure spill over into Monday’s open. However, it is the rebound after that we will be closely watching. If we continue to see deterioration in both fundamental and technical indicators that indicate we are in a bear market and this isn’t just a correction, then we will look to increase both our cash reserve and defensive sector allocations.

As always, we provide a FREE 2nd Opinion Portfolio Review and would be more than happy to discuss your financial planning goals with you – please click here to schedule your meeting, or give us a call at 913.402.6099.

John P. Chladek, MBA, CFP® is the President of Chladek Wealth Management, LLC, a fee-only financial planning and investment management firm specializing in helping families and couples who are not yet retired realize their financial goals. For more information, visit http://www.chladekwealth.com.